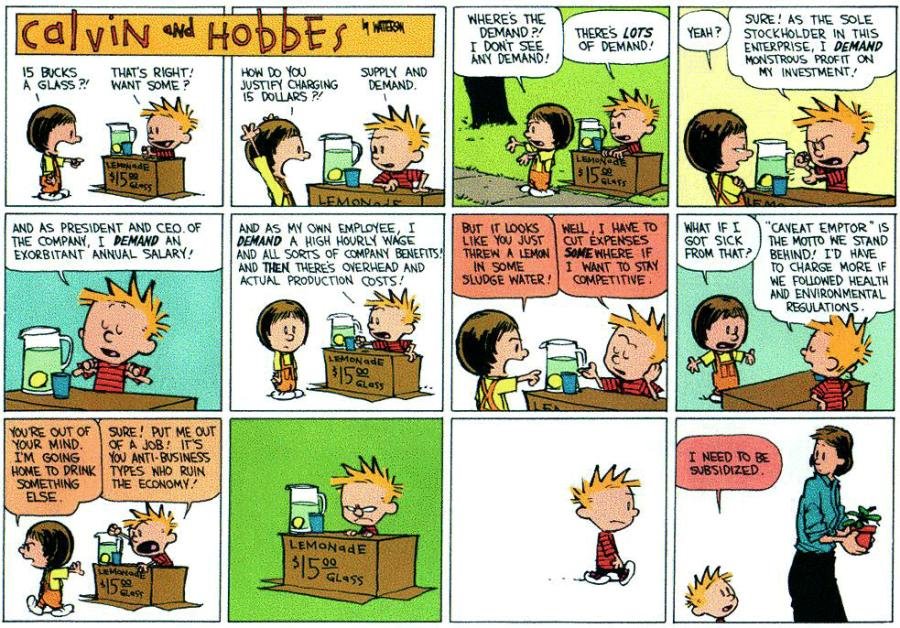

Demand

There are two key components to demand: willingness and ability. You have to be willing to purchase an item and be able to in order to have demand. You might really, really, really want the latest pair of shoes but if you have no money the demand isn't there. Likewise, if you have enough money but do not want the shoes, there is no demand (or at least it is much lower). If the price were to lower, your willingness to spend the money might increase, so as price goes down our demand goes up while if prices go up, our demand goes down. This is the law of demand.

We can show our individual demand and the market demand through the creation of a demand schedule - a t-chart showing where the demand is at various prices. The individual demand schedule takes just one person into account while the market demand schedule is our aggregate demand schedule; it shows the entire market's worth of demand.

|

|

|

In case it's not clear from above, you can see the law of demand in action: as prices go up, demand goes down, and vice versa. This means out demand curve, when graphed, always slopes down.

Using the chart at the right, the graph curve, labelled D1 because it is the initial position of our demand curve, slopes down. As prices go up, the slices demanded per day goes down. When prices lower, the number demanded goes up. This assumes that, in this example, nothing else changes. When circumstances change, the curve will shift and we will have to shift the curve by drawing a new line. This new line will be labelled D2. |

|

If demand shifts by increasing demand, the demand curve will shift to the right. If there is a shift in demand that decreases demand, the curve will shift to the left. All you have to do is draw the same line slightly left or right.

Below are the 7 ways that demand can shift.

Below are the 7 ways that demand can shift.

Income |

Population |

Price Expectations |

Seasonal Changes |

|

When our income goes up, demand goes up. If you make more money, you'll have greater ability to spend more. If you get a raise, your demand will go up. If you lose your job or see a pay cut, you'll decrease your demand as well.

|

As populations increase, demand will as well. This is due to more willingness in the market. With more people, there is more aggregate willingness out there. This is why big cities have greater demand then rural areas with small populations.

|

People change their demand based on what they expect to happen. So if people expect prices to go down in the future, they will lower their current demand. If they expect prices to go up, they will raise their current demand.

|

As the seasons change, our demand will as well. In the summer, for example, you'll increase your demand for popsicles and sunglasses. However, in the winter as it cools down, your demand will go up for hot chocolate and mittens.

|

Consumer Tastes/Preferences/Fads |

Substitutes |

Complements |

|

We all try to keep up on the latest trends and fads, and when something becomes more popular, the demand for it will go up. If the latest diet trend changes, our demand for certain foods may go up or down. These changes cause shifts in demand across markets and across products.

|

Some products have readily available, similar quality substitutes. If they are available, when the price of an item goes up, our demand for the substitute will go up. If the cost of Pepsi doubles, we will find our demand for Coke increases to make up for our demand for Pepsi decreasing.

|

Complements, goods or services that are typically bought and used together, see their demand tied together. So if the price of an item goes up, our demand for it's complement will decrease. Peanut butter and jelly are typically bought and used together, so if a peanut shortage causes peanut butter to be more expensive, we will buy less and therefore buy less jelly.

|

Elasticity

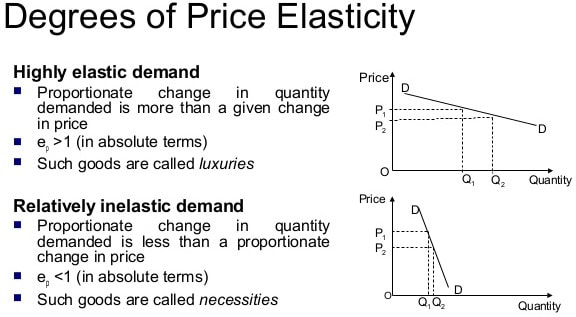

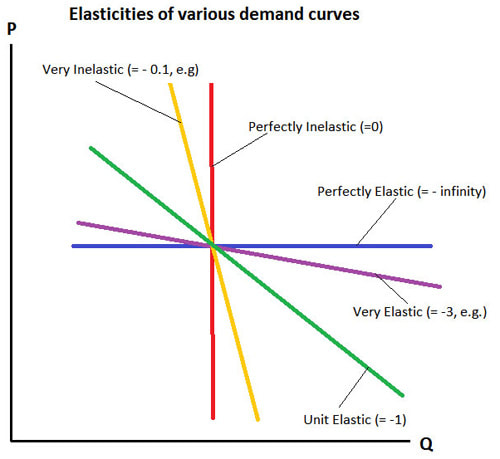

Elasticity is a measurement of how strongly our demand (individual or market/aggregate) reacts to a change in price. Simply put, if prices go up slightly and demand drops, demand is said to be highly elastic for that good or service. Pizza or soda are good examples of highly elastic goods. As price changes, demand quickly changes as well. We end up with a demand curve that is noticeably flatter than the standard demand curve. Luxury items (wants) are much more likely to be highly elastic.

If people do not significantly change their demand when there is a change in price, the demand is more inelastic. More inelastic demand is more vertical (the up and down graph). Items that are necessities (needs) are more likely to have inelastic demand.

If people do not significantly change their demand when there is a change in price, the demand is more inelastic. More inelastic demand is more vertical (the up and down graph). Items that are necessities (needs) are more likely to have inelastic demand.

|

|

To help determine the elasticity of a good or service, there are 4 questions we can ask ourselves.

Are there substitutes? |

Is the product a need or a want? Can the purchase be delayed? |

|

When substitutes are of similar quality and are readily available, demand will be more elastic, since we can turn to substitutes to satisfy our want or need.

|

If we can delay the purchase of a good or service, it is more likely a want. If we cannot delay it's purchase, it is more likely a need. Wants are more likely to be elastic while needs are more inelastic.

|

Does the purchase take up a large or small percentage of income? |

Will time have an effect? |

|

Purchases that take up a larger portion of our income represents more elastic items. We tend to be more willing to delay those purchases and think about if we really want or need them.

|

This one often can't be answered right away. However, over time, more quality substitutes will be produced that allow our demand for specific goods or services to become more elastic over time.

|

Supply

So far we've looked at the demand side of things. That is the side of the consumer - whoever intends to demand a good or service. New we look at things from the supplier side.

Suppliers have incentive to supply. By offering supply, they can make profit. Profit is all the money left after the costs of doing business have been met and a higher profit means a higher incentive to supply. Therefore, according to the law of supply, as prices go up, supply will go up, and as prices go down, supply will go down. When prices are lower, suppliers don't make as much profit so they lose the incentive to supply more of that good or service. Because supply and price are now perfectly related, that means our supply graph will slope upwards. As price goes up, suppliers supply more.

Suppliers have incentive to supply. By offering supply, they can make profit. Profit is all the money left after the costs of doing business have been met and a higher profit means a higher incentive to supply. Therefore, according to the law of supply, as prices go up, supply will go up, and as prices go down, supply will go down. When prices are lower, suppliers don't make as much profit so they lose the incentive to supply more of that good or service. Because supply and price are now perfectly related, that means our supply graph will slope upwards. As price goes up, suppliers supply more.

|

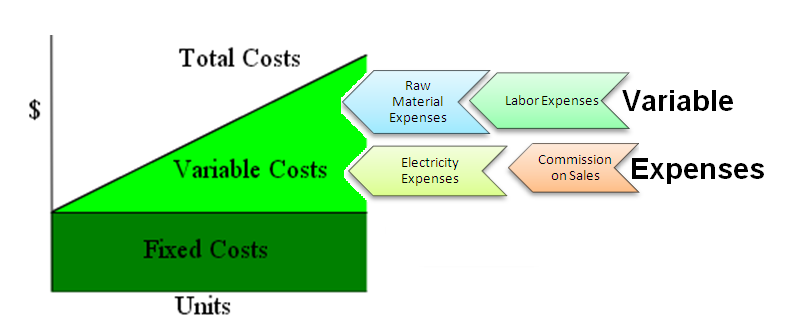

Suppliers, however, typically have costs of doing business and there are two types of costs: fixed costs and variable costs.

Fixed costs create a bottom line of costs that should be easily figured out every month. Variable costs will change as more goods or services are produced, supplied, and sold. |

Fixed Costs |

Variable Costs |

|

Fixed costs are costs that stay the same every month or are predictable month to month. So rent or the cost to pay a salaried manager are fixed costs. Even if you learn that your rent will go up, it is still a fixed cost since it will not change based on how much you use the space.

|

Variable costs change based on the level of production. They are not predictable and depend on what is produced and sold month-to-month. So the cost of supplies like lemons or sugar for lemonade are variable as are the costs to pay hourly employees since you bring them in when it is busy and send them home when it is slow.

|

There are six reasons for suppliers to increase or decrease supply (shift supply). There are three that occur in the market and three that are government driven.

When supply is shifted, the same rules as demand apply. An increase in supply equals a shift in supply that shifts to the right. A decrease in supply equals a shift in supply to the left.

When supply is shifted, the same rules as demand apply. An increase in supply equals a shift in supply that shifts to the right. A decrease in supply equals a shift in supply to the left.

Input Costs |

Number of Suppliers |

Price Expectations |

|

The driving force for suppliers is profit and anything that cuts into profit will cause them to lower supply. When the costs of supplying something go up, supply will go down. However, if it gets cheaper to supply something, profit can increase, leading to an increase in supply.

|

When there are more suppliers in a marketplace, there will generally be more supply. More suppliers enter into marketplaces because they see that others are making profit, so they have an incentive to enter into the market as well.

|

Suppliers are subject to price expectations as well, but it works a bit differently. If suppliers expect the price to go up in the future, they will lower current supply so they can sell more later when the price goes up. If they expect prices to go down in the future, they will increase their current supply to sell while it is more expensive.

|

Subsidies |

Taxes |

Regulation |

|

Government can subsidize businesses to encourage growth into a specific sector. Subsidies, payments by government to increase production, lower the business costs to supply. This means there is more profit to be available since costs are lower. This encourages companies to supply more.

|

Governments can also encourage or discourage supply by raising or lowering taxes. If taxes are low, suppliers spend less on taxes and so have more available for profit, leading them to increase supply. But if taxes are high, it discourages supply since profits will be lower.

|

Government also places regulations onto business, such as safety or environmental regulations. These add costs to businesses - it is cheaper to be able to dump your waste anyone rather than recycle or safely dispose of it. These costs cut into profits and discourage supply as well. Lowering regulations will increase supply.

|

|

|

Practice putting supply and demand together into one money-making adventure by clicking the image to play the Coffee Shop game

|

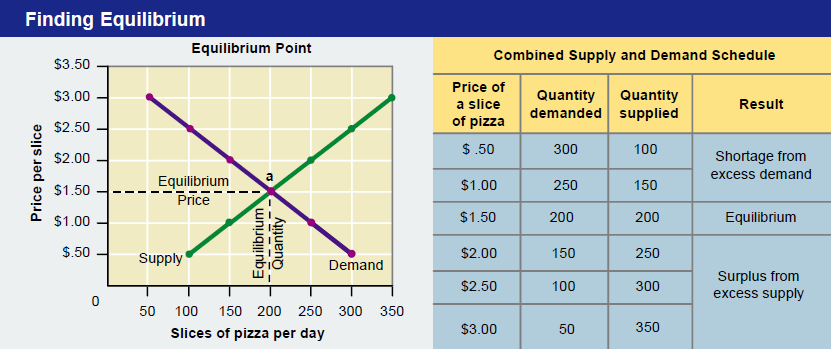

Market Equilibrium

Finally we are putting supply and demand together.

But first... price signals tell consumers and suppliers what to buy and supply. Price signals tells businesses to supply more or less while they tell consumers to demand more or less. This is all driven by competition.

But first... price signals tell consumers and suppliers what to buy and supply. Price signals tells businesses to supply more or less while they tell consumers to demand more or less. This is all driven by competition.

|

|

Competition between buyers pushes prices up. As others are willing to spend more on goods and services (as demand goes up), it sends a signal to suppliers to raise prices.

Competition between suppliers pushes prices down. As suppliers fight for your dollars, they will lower their prices to attract you. Remember the invisible hand? Here it is in action! |

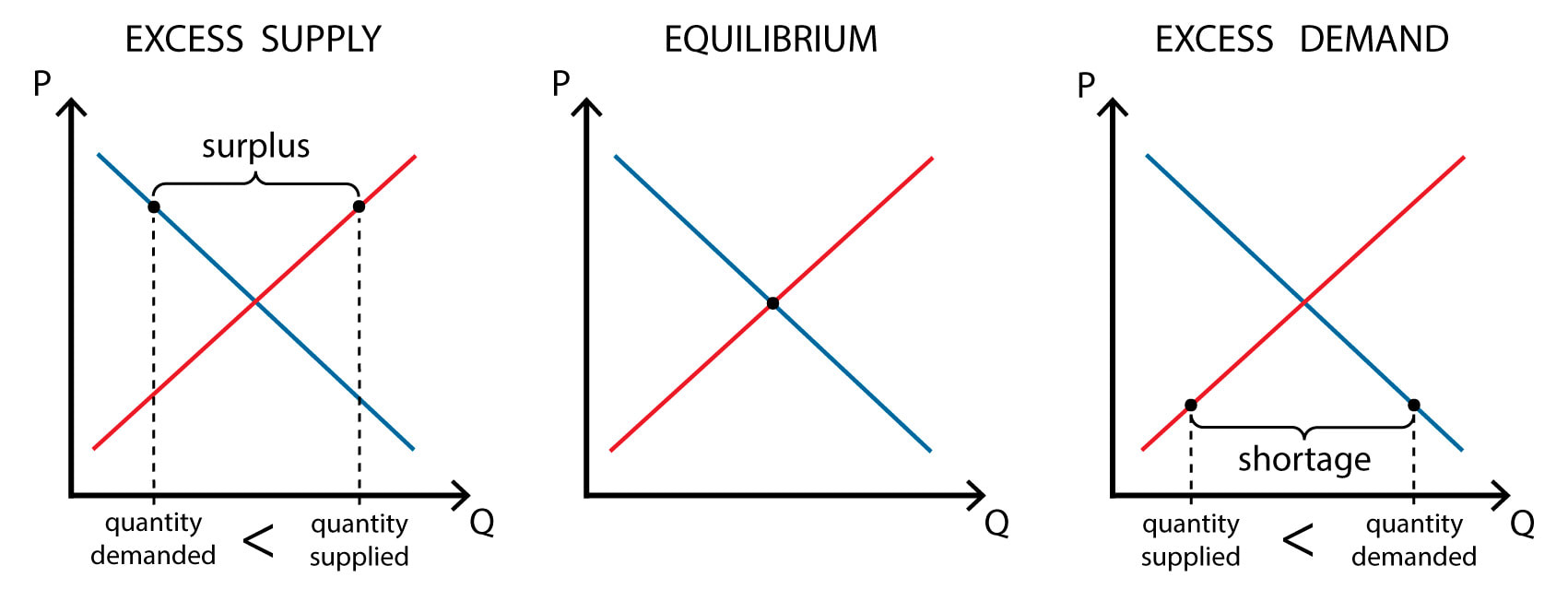

Different circumstances will send different price signals to suppliers and consumers. Low prices tend to signal to consumers, but suppliers receive a lot more signals. For example, when there is a shortage, it tells suppliers to raise the price and raise production since it is below equilibrium price and in higher demand. These are caused by low prices and increased competition between buyers. When there is a surplus, it tells suppliers to lower price and lower production, as there is too much supply and competition between sellers.

If our economy has reached equilibrium, then it has hit the point where supply and demand are perfectly equal. The amount chosen to sell for the market is the exact amount consumers demand at the set price. While this is a rare scenario in reality, this is what suppliers are always striving for. This would be the market clearing price.

|

If an equilibrium can be determined in a market place, the supplier will always strive for it since it means they will not have any unsold goods or services and they will not have missed the opportunity to sell even one more unit to anyone.

|

|

Prices

Marketplaces have different methods of determining prices and the structures in place that help determine prices. It depends on the type of economy chosen by governments (see unit 1) as well as the specific market examined. In the US economy, for example, there are different levels of competition depending on the good or service. The three different levels of competition are perfect competition, oligopoly, and monopoly.

At perfect competition, we assume that there are as many buyers and sellers as want to be in the market and we don't restrict who can be a buyer or seller. This means there are no government barriers, though there may be natural barriers such as start-up costs. In this level of competition, sellers are able to introduce similar products for consumers to choose between and consumers are able to learn about and understand the goods and services they can purchase. All together this is perfect competition and market competition establishes prices.

|

At an oligopoly level, we have higher barriers to entry, which limits the number of sellers. This also has the effect of limiting the number of options available. These limits are due to higher restrictions placed on the suppliers in this market. For example, there are greater regulations on car companies, so there are fewer options and fewer variety within those options. This also means the government may institute some form of price controls to keep a more fair playing field.

|

|

|

|

At the final level, monopoly, there is only one firm. This is due to the extreme barriers to entry. This means there is only one places consumers can turn to so government needs to enact a much more rigorous form of price control. These industries are typically things like the water company or the electric company and are done so because it would be challenging to have multiple electric firms running wires everywhere. There are other examples as well, such as radio stations or government registered patents of monopolies.

|

|

Because of these levels of competition, governments can enact price controls to help support the market. These can be price ceilings or price floors.

|

|

Price Ceilings |

Price Floors |

|

Price ceilings place an artificial cap on what the price can go up to. This means there is a maximum price that can be charged. Price ceilings lead to shortages, since lower prices lead to higher demand and lower supply. Rent control is a prime example of a price ceiling.

|

Price floors set a minimum price that can be given for a good or service. These minimum prices lead to a surplus in the market as suppliers are willing to supply more and consumers demand less. Minimum wage is an example of a price floor - when wages are higher, suppliers (laborers) will supply more hours but consumers (businesses) will demand less workers.

|

|

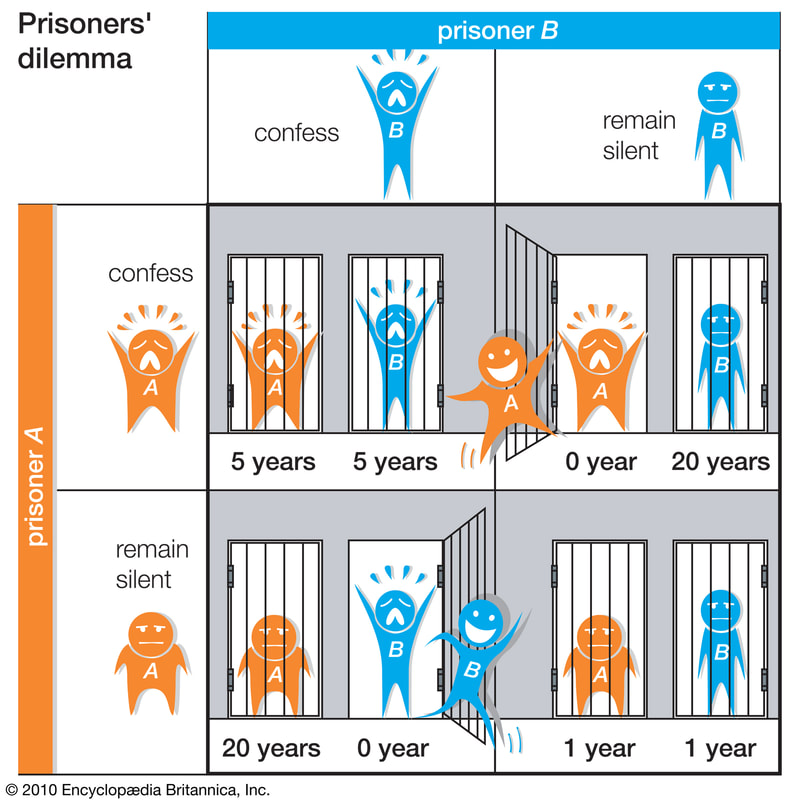

When companies make choices, we can use the prisoners dilemma and game theory in order to help determine how they should or will make choices. While we don't always make the most rational decision, it can tell us how people and companies ought to behave.

Two actors, when placed with a set of scenarios, will often resort to the option that gives them the best, or least worst, option. In the case of the prisoners, the best option is to always confess and take their chance on what the other prisoner will do. No matter what the other prisoner does, by confessing they gain the best outcome for themselves, even if the outcome is not the best cumulative situation for both of the prisoners. |

|

Taken into the real world, companies interact the same way. Two companies can compete with advertisements or by arranging their prices at a specific value. By offering the best option, they can acquire the most customers, but if the other does as well, they may cumulatively lose out. They could be better of with cooperating but in the real world that is called collusion and it is illegal for businesses to collude. Businesses have to operate without knowing what the other company will do, but have to make the assumption that other companies will make the most rational decision for themselves. This should lead both companies to making a decision that isn't necessarily the best all-around, but does offer the best option no matter what the other company does.

Case Study: Minimum Wage

|

As you watch the episode, ask yourself:

What advantages do they have going into this? What disadvantages do they have? What was realistic about their simulation? What was not realistic about their simulation? click the button to watch the episode

|

Alex (left) and Morgan (right) in front of their apartment they were able to rent.

|

When it comes to the minimum wage, if it is set above equilibrium, we will experience a surplus of workers for jobs available, which will mean more unemployment as there aren't as many jobs available.

HOWEVER, if we raise minimum wage and we don't lose jobs, that means we haven't raised it past equilibrium.

HOWEVER, if we raise minimum wage and we don't lose jobs, that means we haven't raised it past equilibrium.