Unit 1: Principles of Economics

Unit 1 is covered by chapters 1, 2, and 3 of the textbook we use.

Assume that this monstrosity isn't an option.

Assume that this monstrosity isn't an option.

|

Answering these three questions will help them decide what they will be doing. If they decide to make tennis balls by hiring people to put them together for adults, they will make different decisions then someone who decided to make potato chips with machines for teens and kids (even if they can use similar packaging).

|

|

Freedom is an individual's ability to make decisions. And I use individual loosely, as it can mean an individual business or corporation. If there is more government involvement, there is less freedom, so the more rules and laws there are the less freedom there is.

|

|

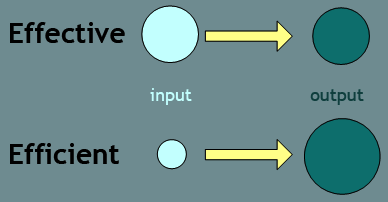

Efficiency is how well resources are used to accomplish something. If it costs less resources (time, money, effort) to complete than someone or something else, it can be said to be more efficient than others.

|

|

|

Security and predictability often go hand-in-hand. There is security when things are more predictable and there is a predictability when we feel secure.

However, that doesn't mean they always go together. Living on a busy street can be very predictable but it's not always secure to have that many cars and people going by. If you have a good job that you aren't worried about losing that is secure, but the job may not be predictable. Finding a map to treasure can be predictable, since it will tell you where all the dangers are, but the path may not be secure. |

|

Equality is when everyone is gets or is given access to the same things. We all have equal access to working for one million dollars for example, but some of us might have an easier time doing so. If the government decided to give everyone the same brand of shoes, that would also be equal. But not all of us might need shoes or be able to wear the same brand, which brings us to...

|

|

|

Equity is giving everyone what they need to be on a level playing field with others. For example, if you picture people who live different distances from school, it might be easier for some to get to school on time. If we give the closest person nothing since they don't need anything and the furthest person a bus pass, both get exactly what they need to make it to school at the same time.

|

|

Traditional economies focus on completing tasks based on custom and ritual. These economies prefer to do things the way they always have. These economies tend to be seen when

These economies tend to be secure and predictable, as you know your role and know what to expect in the economy. However, these economies discourage innovation and provide low opportunities for growth, leading to them being generally poorer.

|

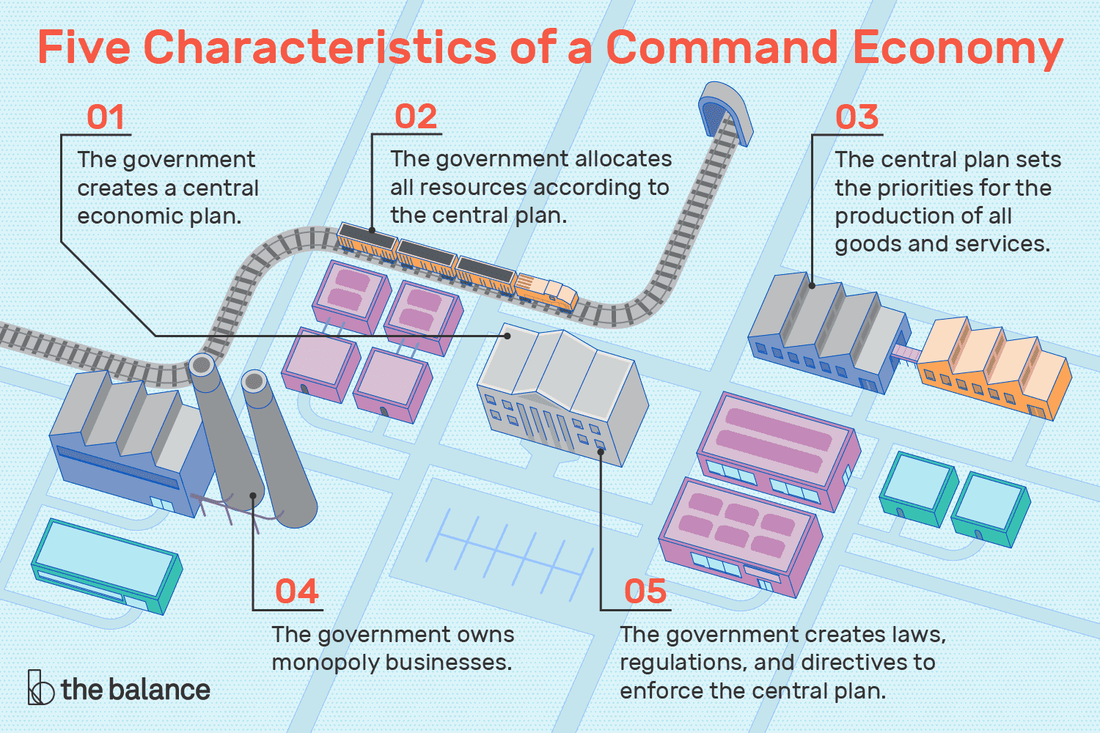

Command economies are designed to have governments make the decisions. These economies are top-down and often need to have large bureaucracies to function.

Command economies, also known as centrally-planned economies, can be efficient as they react to changes quickly. They can also be used to promote equality or equity and you may have more security in a command economy as they tend to focus on getting people what they need. Command economies can also be inefficient, since large bureaucracies are slow to react. They also ignore innovation and you lose a lot of freedom when governments make decisions.

|

Market economies have individuals making the decisions. Government takes a very hands-off approach in a market economy.

In a market economy, individuals have lots of freedoms and since you can acquire more wants there are a variety of goods and services. A market economy can also be efficient, since individuals can each react on their own to changes. On the other hand, market economies completely ignore equality and equity. Not everyone will be able to afford to satisfy their needs and wants and market economies don't help people to do so. This means there is little security as well. Furthermore, market economies have potential for big success but also big loss.

|

|

|

Most countries don't actually use a pure form of any of those economies, however. They all try to balance those values in different ways to maximize the values in ways they prefer. Many economies tend to be a mixture of different elements of each type. Mixed economies are put in place to promote the good qualities of as many values as possible. The USA is a mixed economy; it tends to prefer free market principles while ensuring there are some command elements to prevent disaster and provide safeguards for people.

|

|

In all this, the US government plays a role as well. This is where the command elements present themselves.

Our government offers safety nets, public goods, and regulations. |

|

Safety nets are programs that help people in disadvantaged circumstances. People who don’t make enough to afford their basic needs for example can apply for government food stamps, cheaper housing, unemployment, disability, and so on. These programs help to smooth out the possible large failures of our market economy. These safety nets are paid for by taxes and are often considered entitlement programs because you are entitled to take them if you meet certain requirements.

|

Our government also creates rules and regulations for businesses to operate under. Without them, businesses would seek to cut costs to maximize profits. Regulations can be workplace safety regulations, such as the requirement to wear a hard hat, environmental regulations, like rules on how and where companies can dump their waste, or general rules to ensure workplace stability, like minimum wage or equal opportunity hiring. Without these, companies would cut corners and put workers at risk to increase the money they make.

|

|

Public goods are any goods that would be troublesome to exclude non-payers and burdensome for a private company to take on. Public sidewalks, for example, would be a challenge for a company to maintain and keep in working order. They would also have an expensive time hiring security and ticket collectors if they sought to exclude people who didn’t pay to use them. Public goods are set out by the government to benefit us. In return, we pay a little in taxes to cover their maintenance and costs.

|

|